Loudoun Business Tax Assessment Schedule Changes Effective Jan. 1

Based on the results of a recent benchmarking study, Loudoun County Commissioner of the Revenue Robert S. Wertz Jr., is updating the assessment schedules for most classes of business personal property. These changes are effective beginning Jan. 1, 2026, and impact taxes levied on computer equipment, furniture and fixtures, computer equipment in data centers, heavy equipment, and machinery and tools.

Virginia law gives local governments the responsibility for taxing tangible property. All property within the same classification must be taxed uniformly and assessments must be based on fair market value (VA Code §58.1-3503(B)). The Commissioner of the Revenue contracted with PFM Group Consulting to study assessment schedules used to value business personal property in Loudoun County, compare them with other Virginia counties and cities, and evaluate how closely they correspond to fair market value. That

benchmarking study was completed in October of 2025.

By March 1 each year, taxpayers must declare all business tangible personal property that was located in the county on January 1. Business personal property assessments are calculated based on a percentage of the original cost of the property. The original cost is the total capitalized cost or the cost that would have been capitalized if the expense deduction in lieu of depreciation was elected under §179 of the Internal Revenue Code and includes the complete cost to place each item into service including shipping, freight, installation and sales tax.

To better reflect fair market value of business property, the assessment schedules will be changed as follows.

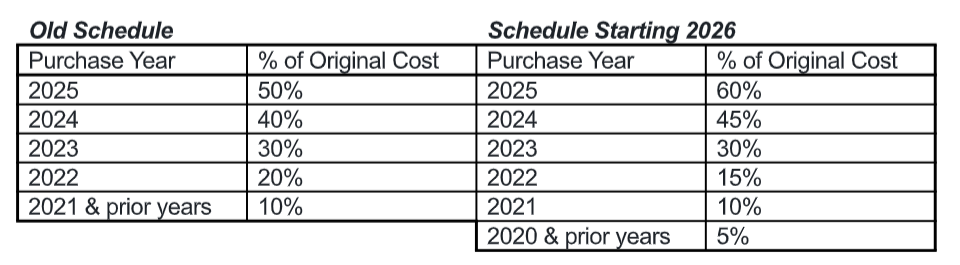

New Business Equipment Classification

Business equipment is a new schedule that combines general computer equipment and furniture and fixtures classes. The schedule has been lengthened and the assessment factors updated.

Beginning with tax year 2026, taxpayers will be required to summarize and report the total capitalized costs by year of acquisition for all business equipment for the most recent year and immediate prior five years in order to properly complete their filings.

As in the past, business equipment with an original capitalized cost of $25 or less can be excluded from reporting. Reportable tangible property includes items that were purchased, leased, gifted or converted from personal to business use, and also includes any tangible property not otherwise classified as data center equipment, heavy equipment, or machinery and tools. Certain farm-related personal property, application software, and household goods that are not used for business purposes are excluded.

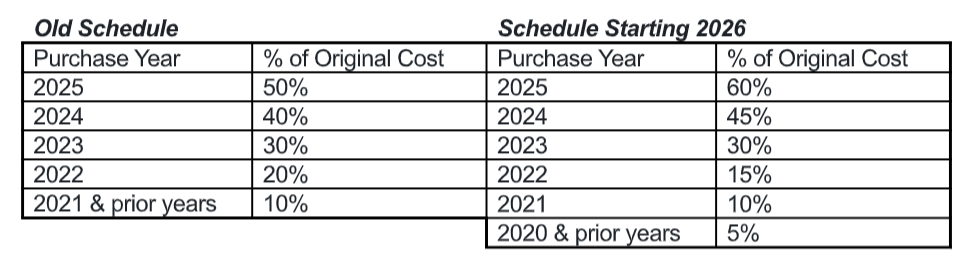

Computer Equipment in a Data Center Classification

The assessment schedule for computer equipment in a data center has been lengthened and the assessment factors updated.

Beginning with tax year 2026, taxpayers will be required to summarize and report the total capitalized costs by year of acquisition for all computer equipment in a data center for the most recent year and immediate prior five years in order to properly complete their filings.

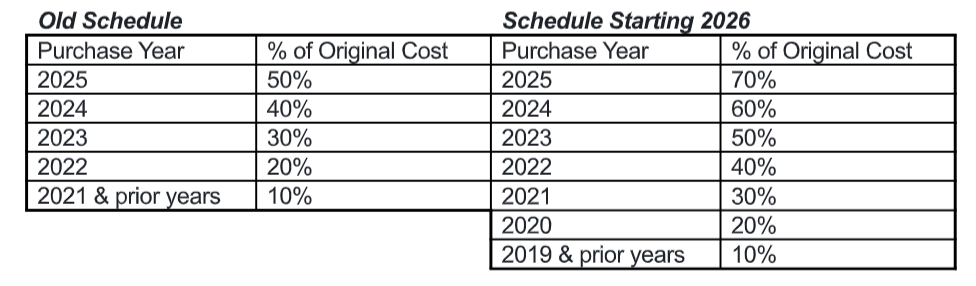

The assessment schedule for heavy equipment has been lengthened and assessment factors updated as reflected below.

Beginning with tax year 2026, taxpayers will be required to summarize and report the total capitalized costs by year of acquisition for all heavy equipment for the most recent year and immediate prior six years in order to properly complete their filings.

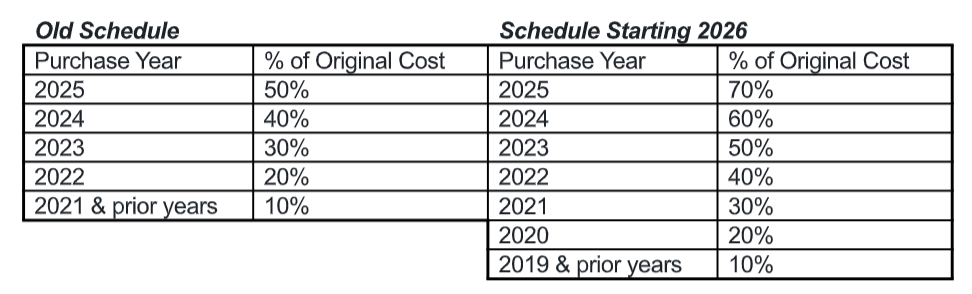

The assessment schedule for machinery and tools has been lengthened and the assessment factors updated.

Beginning with tax year 2026, taxpayers will be required to summarize and report the total capitalized costs by year of acquisition for all machinery and tools for the most recent year and immediate prior six years in order to properly complete their filings.

The public may submit written comments regarding the machinery and tools assessment schedule change (VA Code §58.1-3507(B)) through December 13, 2025, at loudoun.gov/MachineryandToolsComments or by mail to Loudoun County Commissioner of the Revenue, Attn: Robert S. Wertz Jr., P.O. Box 8000, Leesburg, VA 20177.

Taxpayers will receive notices advising them of these assessment schedule changes beginning December 10, 2025.

More information is online at loudoun.gov/cor. To request personalized assistance or clarification, contact the Business Tax Division in the Office of the Commissioner of the Revenue at loudoun.gov/ContactCOR or 703-777-0260, option 2.

Anyone who requires a reasonable accommodation for any type of disability or needs language assistance may contact businesstax@loudoun.gov or 703-737-0260, extension 2 (TTY-711). Three days’ notice is requested.

Comments

Any name-calling and profanity will be taken off. The webmaster reserves the right to remove any offensive posts.